User Tag List

Results 16 to 30 of 33

20Likes

20Likes-

Mon, Aug 25th, 2014, 10:01 PM #16Canadian Genius

- Join Date

- Apr 2011

- Location

- West Vancouver, BC

- Posts

- 7,008

- Likes Received

- 11041

- Trading Score

- 368 (100%)

Thank you everyone for your responses/input. I guess I"m feeling a little nervous investing my money vs having my money in a condo, which, in my area is guaranteed good investment. @blueeyetea ......my credit union wants 1.14% of the investment as a 'management fee', which in my Mom's case is a whole lotta money considering she won't be actively trading stocks, more like a one-shot investment and then not touch it.....a big rip off IMO.

-

-

Mon, Aug 25th, 2014, 10:54 PM #17Canadian Genius

- Join Date

- Apr 2011

- Location

- West Vancouver, BC

- Posts

- 7,008

- Likes Received

- 11041

- Trading Score

- 368 (100%)

here's an article I came across regarding seniors investing in dividend growth stocks.....

http://www.theglobeandmail.com/globe...ticle18593525/

-

Sun, Sep 7th, 2014, 04:16 AM #18My comments in bold above.

Originally Posted by MillieH

Originally Posted by MillieH

Last edited by secret aging man; Wed, Sep 10th, 2014 at 04:00 AM.

-

Sun, Sep 7th, 2014, 05:43 AM #19It's possible to get around 4% dividend yield on stocks conservatively. You might have problems finding/buying quality stocks at this time, because most stock valuations are too high to justify holding 100% of your nest egg in stocks, especially if markets crash (as they will eventually) and you need to access money for emergencies. Originally Posted by redhdlois

For example, if you are investing $500,000 to get 4% return, you would have gross dividend income of $20,000 annually. If these dividends are from Canadian stocks, each year you would need to pay income tax on $10,000. Suppose your marginal tax rate is 25% (lower than if you were working) - you would still owe CRA $2500 in extra income tax. The leftover $17,500 is available to pay rent and utilities for one year. You would need enough in extra savings (or draw down from your condo recently sold) to provide for basic necessities until you can collect other pension income (CPP after age 60, OAP at 65) to help pay for food and other living expenses.

The dividend income from US stocks would be taxed fully, I believe. But the US markets (NYSE, NASDAQ) give greater diversity (Canadian stocks are mainly concentrated in Financials, Oil & Gas, Mining) and they have risen much faster than the Canadian market during 2012-2014 (thus it is better to invest in Canadian, US and even some international stocks as you slowly gain confidence in DIY investing). The hope is that in rising markets you would be able to have your investments grow nicely and cash in some of your stocks to meet your additional expenses or pay for luxuries. And both Canadian and US stocks when sold would qualify for capital gains during income tax filing time, with only 50% of the gains taxable.Last edited by secret aging man; Wed, Sep 10th, 2014 at 03:58 AM.

-

Fri, Jan 16th, 2015, 05:36 PM #20momof5boys

- Join Date

- Sep 2010

- Location

- Western Canada

- Posts

- 2,611

- Likes Received

- 3514

- Trading Score

- 509 (100%)

OK, I'm muddling through retirement readings seeing as my hubby is nearing retirement (he turns 62 this year). I'll be 55 when he's 62. He's planning on retiring at 65 and collecting CPP (he'll get near the max) as well as OAS. We also have a bunch of RRSP and we plan on converting about 100K into a RRIF when hubby turns 65 and then using my age for minimum withdrawals.

If I am reading the CRAs website correctly, I'll be entitled to an allowance from age 60 to 64 if my hubby is collecting the OAS and GIS. We plan on keeping his income at a low level so this will happen. We are used to living on little as our home is paid off.

Am I missing something?

-

Sat, Jan 17th, 2015, 08:57 AM #21Smart Canuck

- Join Date

- Dec 2009

- Location

- Calgary

- Posts

- 3,737

- Likes Received

- 19634

- Trading Score

- 1 (100%)

Mom of 5 boys-I thought that allowance was only if your husband was no longer living?- but you may be right if the GIS is involved. You will get your own OAS when you are over 65 as they are gradually changing the age up to 67. At 65 you would get your own CPP if you paid in and I believe some type of survivor benefit based on your husbands contribution should you outlive him. But I am no expert in interpreting the govt websites. There is a guy called dogger 1953 on Canadian Money forum( under retirement) who is retired from CPP and if you post your general questions he will answer them. Or you can privately hire him at something like $25 per calcualtion to figure out the best time for you and your DH to receive your CPP/OAS. He knows his stuff.

Last edited by lizzie bargain; Sat, Jan 17th, 2015 at 09:03 AM.

-

Sat, Jan 17th, 2015, 09:55 AM #22mandolinatou

- Join Date

- Dec 2008

- Location

- Montreal

- Posts

- 411

- Likes Received

- 918

- Trading Score

- 1 (100%)

If you don't understand the stock market you shouldn't be investing in dividend stocks..or while reading you could dabble with 3-5% of what you have to invest. Originally Posted by redhdlois

I started really young and got both very lucky and very unlucky with dividend funds. I recently sold my favorite fund because it's oil based. It made up for my two very bad losses....and I didn't want to go in the negative if oil keeps going lower. Roughly you have to invest in companies with good management, low debt levels, decent P/E, who have a product/service that is going to continue selling. If you don't know how to determine these facts you don't belong in stocks. You could instead invest in dividend paying ETFs. Anything can happen to the market. I started by investing roughly 1000 dollars in 5 companies 3 of which were dividend companies. One company offering a 10% dividend went under. I hadn't thought about their business model and they hadn't kept up with the changing economy so that was my mistake. Another had an accounting scandal and it's lost roughly 90% thats their mistake. Now it may go back up but it may go under as well and I think I should get a little more if it goes bankrupt than if I sell it now as it owns valuable property/machinery and has little debt. The last one went up 165% and paid a 4.5% annual dividend monthly which worked out to roughly 10% on my original investment. I think the money invested helped me understand the market better. My other two non-dividend stocks did really well. I sold one of them recently after a 75% gain. When buying stocks some will lose and some will gain.

I recommend anyone interested in self directed investing in the stock market start a fake stock account on google, take a pretend 10,000 and buy the investments you want to buy, estimate a 10 dollar per transaction fee, and watch what happens.

If you have under 50,000 to invest in a self directed account, you should be starting with ETFs....or starting with a very small portfolio you can afford to lose.

I am watching the market everyday now as I suspect we are either at the start of a bull market (which would be great) and the increased construction contracts are a good sign for that. Alternatively we may be nearing a bad crash on the faulty assumption that we're due to upward momentum. The market has never behaved exactly like this market but we've never had as enormous of a retirement population legally mandated to start pulling a decent % of their retirement accounts. So my point is anything can happen so start slowly and read a lot. Be greedy when others are fearful and fearful when others are greedy! Good luck.

-

Sat, Jan 17th, 2015, 10:17 AM #23Smart Canuck

- Join Date

- Dec 2011

- Location

- Ottawa

- Posts

- 2,553

- Likes Received

- 7674

- Trading Score

- 1 (100%)

I would like to hear from people who are retired and just living off of CPP and OAS..no work pension!! My husband and I do not have a work pension, our house has been paid since we were 40, we have no debt, we are both 53...we have RRSP's, TFSA but we still have 3 children living at home..we paid(paying for 3 universities, with children paying half) oldest graduated and is working for the govt..other 2 are still in school..I was laid off so it's just my husband working right now ( on contract) which means no benefits....Everything is great now, but just want to know how it will be with no work pension...thanks!!

-

Sat, Jan 17th, 2015, 10:19 AM #24Smart Canuck

- Join Date

- Dec 2011

- Location

- Ottawa

- Posts

- 2,553

- Likes Received

- 7674

- Trading Score

- 1 (100%)

Great thread by the way!!

-

Sat, Jan 17th, 2015, 11:05 AM #25Smart Canuck

- Join Date

- Dec 2009

- Location

- Calgary

- Posts

- 3,737

- Likes Received

- 19634

- Trading Score

- 1 (100%)

SL-I can't speak personally but the max CPP per month is $1065( if you worked 40 years and put in the max) and max OAS is 563.74. If you and your DH each got the max( and it sounds like you may not with the layoff) your max income would be $39,000. Only you know if you could live on this minus your child expenses and supplemented by your RRSP and TFSA. My daughter's grandparents recently retired-their income is approx 30,000 per year from just CPP/OAS and they just qualified for a subsidized apt in Alberta where they will pay 30% of their gross monthly income for rent- currently they are on a waiting list for this subsidized senior apt. Here most people with assets cannot qualify for rent subsidy, but certain assets are not counted against you. They also get free healthcare and senior's Blue Cross here which includes some dental and vision care, Rx etc. Not sure the programs in Ontario. I think it is even trickier for one person to live on a single OAS and CPP should they be unmarried or their spouse pass away before them.

My Mum until recently was living alone on partial CPP, OAS and GIS. She owned her own place in the country and she is very frugal-she figured she could live comfortably on 18,000-20,000 per year. She did have savings as a back up or for travel or emergency car or roof replacement. Now that she is going to be looking to rent a place in the city it will be much harder to live on her monthly income-she will have to dip into her savings each month to supplement.Last edited by lizzie bargain; Sat, Jan 17th, 2015 at 11:07 AM.

-

Sat, Jan 17th, 2015, 12:11 PM #26Junior Canuck

- Join Date

- Jan 2009

- Location

- Nanticoke

- Posts

- 418

- Likes Received

- 426

- Trading Score

- 0 (0%)

So...if you are not working or receiving CPP disability benefits when your husband turns 65 and you are between 60-64 - you can apply for a supplement. HOWEVER, if your husband is receiving CPP and OAS - the amount you get will be taken off his income - maybe not the whole amount - but his income will be decreased when that happens. You could always call them and ask if they could give you some figures. Originally Posted by momof5boys

You also might want to talk to an investment counsellor for the RRIF and how that impacts the CPP and OAS. I think the OAS will be affected when you have other income. The RRIF will not be taxable if it comes out of the RRSP - but it is still an income

-

Sat, Jan 17th, 2015, 12:21 PM #27Junior Canuck

- Join Date

- Jan 2009

- Location

- Nanticoke

- Posts

- 418

- Likes Received

- 426

- Trading Score

- 0 (0%)

DH and I have been self employed forever! So - no company pension and not a lot of savings. DH took early pension at age 60 - because he was facing a low pension anyway (under $300/month) so when we worked out the numbers, with the few dollars lower, at an earlier age, he would actually catch up to the same amount by age 71 - so getting it for an extra 5 years seemed resonable to us. Originally Posted by SavvyLady

At this point, I would say we are managing - all bills are paid and food is on the table - certainly no extras abound. We are going to wait for the real estate market to change (for the better) and infuse a little more cash into the income flow

-

Sat, Jan 17th, 2015, 12:45 PM #28Smart Canuck

- Join Date

- Dec 2009

- Location

- Calgary

- Posts

- 3,737

- Likes Received

- 19634

- Trading Score

- 1 (100%)

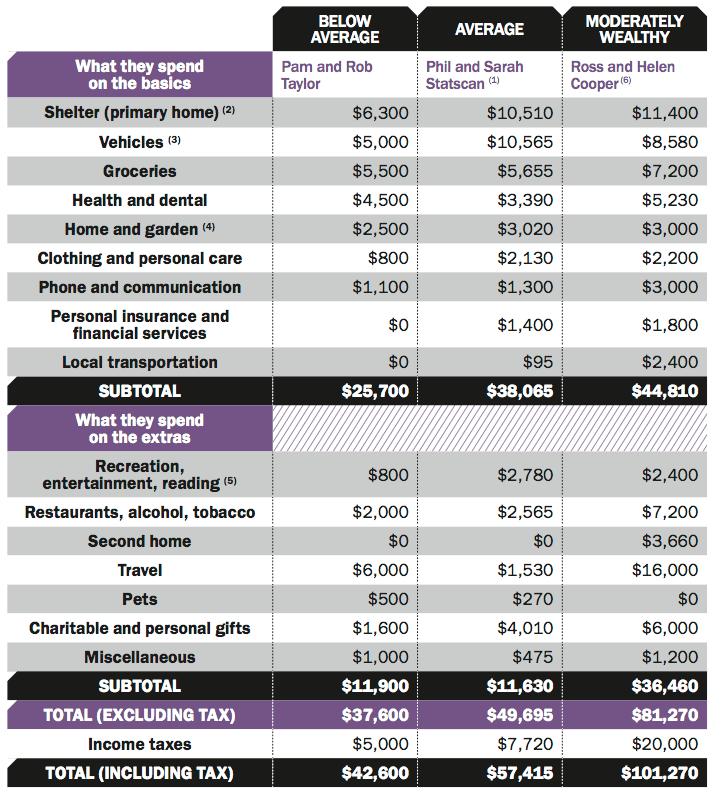

From Moneysense Magazine Dec 2014-can also read the whole article online.

The cost of retiring well

Below we show how much three retired couples spend each year on both the basics and the extras that can make life more fun. Two are real Canadian families— the Taylors and the Coopers—while the fictional Statscans are based on the average spending amounts reported by senior couples in Canada.

-

Sat, Jan 17th, 2015, 01:01 PM #29Canadian Genius

- Join Date

- Apr 2011

- Location

- West Vancouver, BC

- Posts

- 7,008

- Likes Received

- 11041

- Trading Score

- 368 (100%)

Thank you for your input ! I have pretty much decided investing in the stock market is not a wise idea. LIke you mentioned, I have no experience in it, so why start now. Setting up a 'fake' account is a great idea, but for me personally, I don't think I have the time or desire to use my time doing that unless I were to eventually start going it 'for real'.I personally think the market is severely over inflated and is due for a correction. There are so many changes happening in the world today, countries are in financial collapse and the effects will ripple to other countries. I think I will play it "safe" and just buy a place to live and seek some independent advice on how to manage my finances. This is when a crystal ball would come in handy lol Originally Posted by mandolinatou

-

Sat, Jan 17th, 2015, 01:15 PM #30Junior Canuck

- Join Date

- Jan 2009

- Location

- Nanticoke

- Posts

- 418

- Likes Received

- 426

- Trading Score

- 0 (0%)

Please don't use the bank or credit union as your financial advisor - as Gail Vaz Oxlade says - they are not working in your best interests. Use an independent financial advisor. Originally Posted by redhdlois

My opinion on the renting vs bying question is - it is dependent on your income and how much you want to tie up in the real estate. If you want to have some equity for 40 years down the road when you might have to go into a care home - you might want to go with this option.

However, home ownership - as we all know - doesn't just involve the mortgage. Among other costs are - condo fees, taxes, upkeep/repair and maintenance etc

Send PM

Send PM

Thread Information

Users Browsing this Thread

There are currently 1 users browsing this thread. (0 members and 1 guests)